In Mt. Vernon, the strongest offer is the one that balances price, terms, timing, and closing confidence.

When the offers start coming in on a home you’re selling, it’s incredibly easy to just look at the highest number on the page and assume it’s the winner. But, when it comes to real estate in Mt. Vernon, Illinois, the most successful sale is rarely just about the headline price. It’s about finding the offer that actually carries you smoothly across the finish line.

Table of Contents:

- Why the highest offer isn’t always the best

- Breaking down the anatomy of an offer

- Price vs. Net proceeds: What sellers walk away with

- Financial strength: Cash vs Loan offers

- Contingencies: The hidden deal-makers or breakers

- Closing timeline and flexibility

- Buyer behavior and communication

- How a local expert helps you choose the right offer

- FAQs

- Choose the offer that works best for you

Here’s what to watch out for to confidently pick the right package for your move.

Why the highest offer isn’t always the best

One of the most useful tips for selling a house is to judge the full offer package, not just the highest price. Seeing a big number on an offer for your listing is a great feeling, especially after weeks of cleaning, staging, and hosting home showings. But it’s important to remember that the initial price is just the starting line.

A buyer can easily submit a proposal that sits well above the asking price, but that big number loses its magic quickly if the mortgage pre-approval is shaky, the bank appraisal comes in low, or the home inspection turns up a stressful list of costly repairs.

Sometimes, a slightly lower price turns out to be the smarter, safer path for a family when the overall terms are stronger. There’s a lot of peace of mind in a clean contract that comes with verified cash funds, fewer conditions, or a move-in date that aligns beautifully with the next transition.

On the flip side, a much higher offer may still be worth serious consideration, but sellers should look closely at the risks behind it, especially if it leaves them waiting for the buyer to sell another house first, or if it feels like a setup for a tough renegotiation after the inspection.

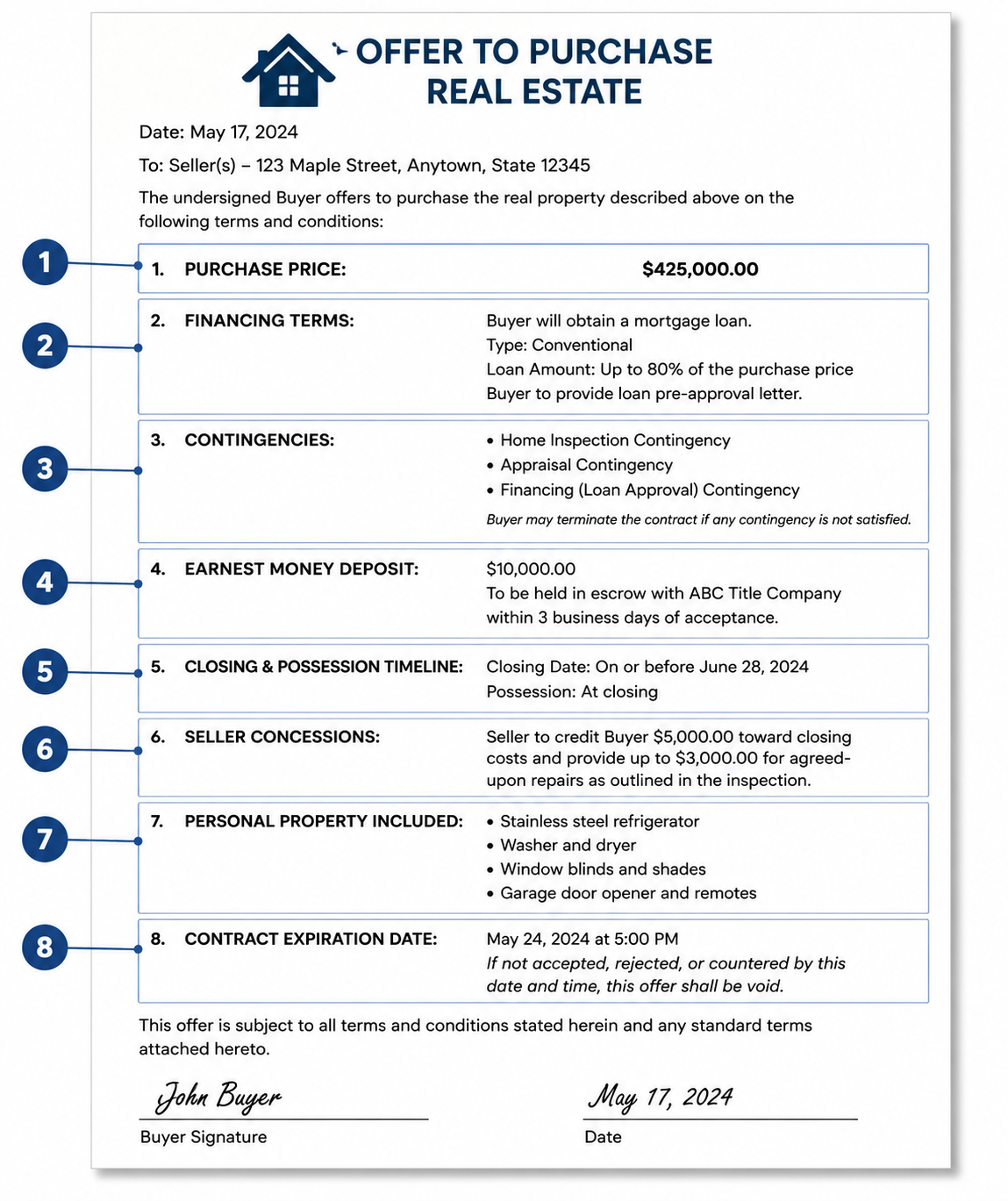

Breaking down the anatomy of an offer

A purchase offer has several moving parts, and each one can affect how smooth the sale feels for a Mt. Vernon seller.

- The purchase price shows the headline dollar amount the buyer promises to pay before any fees, credits, or closing adjustments are figured in.

- The financing terms detail whether the buyer is paying in cash or obtaining a mortgage, such as a conventional, FHA, VA, or USDA rural housing loan.

- The contingencies act as protective rules that give the buyer a safe way to back out or change terms if the home fails an inspection, appraises low, or misses bank approval.

- The earnest money deposit is a good-faith sum of money that the buyer places in a secure account to demonstrate they’re serious about completing the deal.

- The closing and possession timeline establishes the exact date ownership transfers to the buyer and the specific time the keys are handed over.

- The seller concessions are specific requests in which the buyer asks the seller to help pay closing costs, provide repair credits, or cover other expenses from the final payout.

- The personal property section itemizes additional items outside the physical house (such as appliances or window blinds) that the buyer wants included in the sale.

- The contract expiration date sets a strict deadline for the seller to accept, reject, or counter the offer before it automatically becomes void.

Pro Tip: Think of earnest money as a security deposit for your home sale. This cash is held by a neutral third party during the deal, and if the buyer walks away for a reason not covered by their contract protections, you may be entitled to keep some or all of it, depending on the contract terms and applicable law. A larger deposit is a great sign that a buyer has skin in the game and is fully committed to making it to closing day.

Price vs. Net proceeds: What sellers walk away with

While the initial sale price usually gets the most attention, the net proceeds—the actual cash left over at the end—are what truly matter for the bottom line. This final walk-away number is what remains after subtracting transaction costs like a mortgage payoff, real estate commissions, Jefferson County title fees, pro-rated property taxes, and agreed-upon repair credits.

This is where a simple home valuation guide can help you connect the asking price, offer terms, and final payout.

Setting multiple offers side by side makes it easy to see how different contract terms quietly reduce that final payout. For instance, when a buyer asks for closing cost assistance, your net proceeds drop dollar-for-dollar. A delayed closing date also drains cash by forcing you to keep paying for local utilities, insurance, and interest, while adding extra conditional clauses simply gives a buyer more opportunities to renegotiate the price or walk away entirely.

To see how this works in a real-world scenario, look at how a higher offer with heavy concession requests actually nets less cash than a lower, cleaner offer:

| Offer A (Higher price) | Offer B (Cleaner offer) | |

|---|---|---|

| Offer price | $450,000 | $435,000 |

| Closing cost help for buyer | – $12,500 (requested help) | – $0 |

| Repair credits | – $8,000 (agreed to after inspection) | – $0 (bought as-is) |

| Agent commission (6%) | – $27,000 | – $26,100 |

| Estimated title, recording, and closing fees | – $3,200 (title policy and recording) | – $3,200 (title policy and recording) |

| Property tax adjustments | – $5,500 (Illinois tax credit to buyer) | – $5,500 (Illinois tax credit to buyer) |

| Estimated net payout | $393,800 | $400,200 |

Pro Tip: The most reassuring way to handle this process is to ask your agent for an official seller net sheet. It organizes competing offers into clear columns just like the example above, stripping away the distraction of the big numbers so you can see a realistic estimate of the actual cash you will walk away with.

Financial strength: Cash vs Loan offers

Cash and loan offers can both work for Mt. Vernon sellers, but the stronger choice depends on proof of funds, lender strength, and closing risk.

In Mt. Vernon, Illinois, real estate cash offers may reduce risk, but they don’t automatically make every term seller-friendly. You’ll still want to see a proof-of-funds letter from the buyer’s bank confirming that the funds are available. It’s also important to remember that cash buyers can still ask for long inspection timelines or large repair credits, so the offer should be viewed as a whole package.

Instead of using liquid cash, most buyers need to borrow money from a bank to purchase a home. While a loan adds a few extra steps to the process, a financed offer can still be a highly reliable path to a sale as long as the buyer is prepared with a solid pre-approval letter.

To see exactly how these two paths compare, look at how cash and loans handle the main contract steps:

| Cash offers | Loan offers (Mortgages) | |

|---|---|---|

| Bank approval | None needed. | The bank must verify the buyer’s credit, income, and job. |

| Home appraisal | No lender-required appraisal, although a cash buyer can still choose to order one. | A bank appraiser checks the home’s value before lending money. |

| Time to close | Fast, often within a few weeks if title work and any inspections are ready. | Standard, usually taking 30 to 45 days for bank paperwork. |

| Main risk | You must confirm the buyer has the cash. | The loan could fall through, or the appraisal could come back low. |

The main thing to watch out for with loan offers is an appraisal gap. If a buyer offers a price that is well above what neighborhood homes have sold for, the bank might value the home at less than that offer price.

Because real estate in Mt. Vernon, Illinois, has a unique mix of custom homes, historic properties, and land that doesn’t always fit into a simple formula, low appraisals can happen. A good contract will state ahead of time whether the buyer will pay the difference in cash, ask you to drop your price, or cancel the deal.

Contingencies: The hidden deal-makers or breakers

Contingencies are safety rules built into a contract that give a buyer a defined way to check the condition and value of a home before the sale is final. While they’re a standard part of many deals, a strong offer will have short, tight timelines so your sale doesn’t get stuck in limbo.

The home inspection contingency gives the buyer a set number of days to have professionals check the roof, structure, and systems. Afterward, depending on the contract terms, the buyer can accept the home as-is, request repairs or cash credits, or cancel the deal and get their deposit back. This is a normal part of selling a home, especially for older houses or rural properties around Mt. Vernon with private septic systems, wells, or extra land.

A home sale contingency means the buyer is making their purchase dependent on selling their current home before they move forward with buying yours. These are fairly common, but you need to check how safe the buyer’s own sale really is. To figure out the risk, look at a few simple questions:

- Is the buyer’s current home already under contract with another buyer?

- Have they already made it past their own home inspection?

- Is the buyer paying with cash or using a standard loan?

- How long does the buyer have to officially close on their house?

- Do you have a kick-out clause that lets you accept a better offer if one comes along?

Beyond inspections and home sales, you should also watch out for financing and appraisal contingencies. A financing contingency gives the buyer a way out if their bank loan gets denied within the timeline allowed by the contract. An appraisal contingency lets them renegotiate or cancel the contract if a bank appraiser decides the home is worth less than the agreed purchase price.

Closing timeline and flexibility

A strong offer should match your next move, from the closing date to when you’re ready to hand over the keys.

When you look at an offer for real estate in Mt. Vernon, Illinois, the closing date on that paper will play a major role in shaping your moving plans, your stress levels, and your wallet, making the right timeline just as important as the price.

A fast closing date can be a major advantage if your house is already empty or you’ve already packed up and moved. Wrapping things up quickly may help you avoid paying for extra months of property taxes, utility bills, and insurance on a place you are not even using. In many cases, cash buyers or people with strong financing already in place are the ones who can close the fastest.

On the other hand, a longer or more flexible timeline can be a lifesaver if you still need to find your next home, pack up years of memories, or just coordinate a busy family move.

Pro Tip: If you need extra time to pack but don’t want to lose a great buyer, ask your agent about a post-closing occupancy agreement. This is a common setup that lets you officially sell your home, get your cash, and then rent the house back from the new owner for a few extra weeks so you can move at your own pace.

Buyer behavior and communication

While the written words on a contract are the legal rules of the deal, the way a buyer and their agent act right now gives you a great preview of what the next few weeks are actually going to feel like. As you look over an offer, you can actually learn a lot about what a buyer will be like to work with just by watching for a few simple signs:

- The initial response time: If they get back to you quickly and respectfully during these first talks, it’s a great sign that they’ll respect your timelines all the way to closing day.

- Financing clarity: A prepared buyer will always hand over clean proof of funds or a solid pre-approval letter right away, without making you or your agent chase them down for it.

- Document quality: A neatly organized contract that’s free of sloppy mistakes or missing signatures shows that they take you, your home, and the whole deal seriously.

- Negotiation tone: A buyer who treats these initial price discussions like a team effort is much more likely to be reasonable later on if a minor issue pops up during the inspection.

Pro Tip: Your agent’s relationship with the buyer’s agent matters more than you think. When both professionals have a great working bond, they can usually smooth over minor hiccups behind the scenes with a simple phone call before those issues ever turn into a headache for you.

How a local expert helps you choose the right offer

A local Mt. Vernon expert can help you compare the full offer, spot risks, and negotiate with a clearer plan.

At the end of the day, sorting through offers is a mix of looking at the math, balancing the risks, and figuring out what makes the most sense for your future. Having a trusted local professional by your side means you get the real story and the right context. It lets you weigh all your options without ever feeling rushed or pressured into making a choice that doesn’t fully fit your family’s big picture.

When you partner with an expert who knows real estate in Mt. Vernon, Illinois, inside and out, you get an advocate who understands how local buyers are approaching the market, how unique neighborhood homes can affect bank appraisals, and how contract details may play out in Jefferson County.

A dedicated local guide can help you compare offers, verify buyer strength, spot contract risks, and negotiate counter-offers that protect your equity and moving timeline.

FAQs

What does “as-is” mean when selling real estate in Mt. Vernon, Illinois?

Selling “as-is” means the property is sold in its current condition, and the seller is not agreeing upfront to make repairs before closing.

However, the buyer can still request a home inspection, and the seller must still complete required Illinois disclosure forms unless an exemption applies. Illinois’ standard disclosure language also makes clear that an “as-is” sale does not erase the parties’ disclosure rights and duties.

What is a backup offer, and should Mt. Vernon sellers consider one?

A backup offer is a secondary contract that may move into first position if the first buyer walks away, depending on how the backup agreement is written. Keeping a backup offer in place is a smart way to protect a sale from unexpected inspection or financing issues without having to fully restart the marketing process.

Can a seller accept another offer after already accepting one in Illinois?

In most cases, a seller cannot simply cancel a signed contract just because a higher or better offer comes along later. A new offer can usually only be accepted as a backup offer, or handled according to the specific terms of the existing contract, such as a kick-out clause if one applies.

Illinois real estate attorneys commonly note that the answer depends on the contract language, especially where contingencies or kick-out provisions are involved.

Can a seller negotiate after the home inspection in Illinois?

Yes, if the contract includes an inspection contingency, the buyer can request physical repairs, price reductions, or cash credits based on the inspector’s findings. The seller has the right to agree, counter, or decline those requests, subject to the deadlines and terms in the contract.

How do sellers compare investor offers with traditional buyer offers?

Investors may offer fast cash, zero contingencies, and an as-is sale, but they typically offer a lower purchase price. Traditional buyers may pay a much higher price for the home, but the sale often involves bank loans, appraisals, and standard inspection timelines.

Choose the offer that works best for you

Sorting through offers can feel a bit overwhelming, but focusing on the timelines and terms that bring the most peace of mind is what truly leads to a smooth transition. Partnering with a calm, experienced guide ensures the entire process stays straightforward.

Cory Capps, owner of Capps Realty, is a lifelong local who has been helping neighbors comfortably navigate real estate in Mt. Vernon, Illinois since 2017.

When you’re ready to have a relaxed, no-pressure conversation about your next move, you can reach Cory at 618.231.6548 or via email.